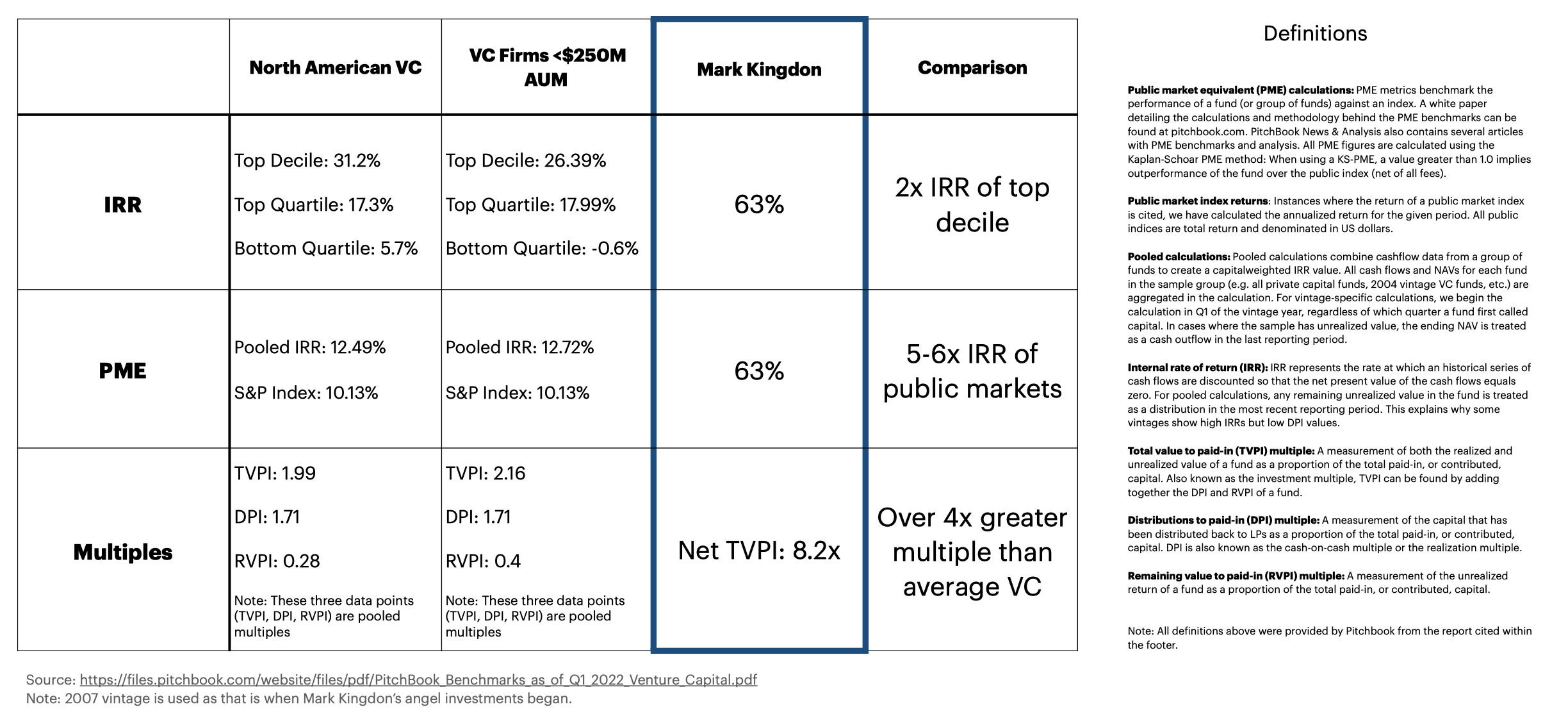

TheRealReal is a luxury marketplace for high-end European luxury brands – and now art. The luxury goods market is a $300+ Billion market worldwide (original sale not re-sale). I guess that qualifies as a rich niche.

TheRealReal solves two real customer problems. Let’s say you regularly buy the latest Loubies at $1000+ a pop. You wear them a few times to parties or a benefit then what do you do with them? You can let them gather dust in the closet, give them to charity for a tax write-off or sell them on TheRealReal and recapture some of the original value. If you’re a savvy shopper, you do the latter. That’s the consignor story. For the consumer, TheRealReal makes luxury accessible — great brands at discounts up to 90% off original retail. You can find a (pre-owned) Chanel dress on TheRealReal for the same price as a (new) Diane Von Furstenburg wrap at Bloomingdales. Great value! If you’re a dude, it’s kind of like buying a Ferrari 458 for the price of a BMW 5 series. Get it? Plus all the product has been vetted by experts so you know it’s the REAL deal (this is a big market differentiator by the way).

Last month, Julie Wainright (the founder and CEO of TheRealReal) walked the board through her three-year plan outlining a huge and achievable future. It wasn’t just a walk, it was a joy ride. We applauded loudly and often; then resoundingly approved the plan. As an investor, there is nothing more gratifying than a company with all metrics dramatically up and to the right. #itsabeautifulthing (VC investors include Greycroft, Canaan Partners, e.ventures, Novel TMT Ventures and Interwest).

While Julie was mapping out the future, I looked back at her 2011 pitch deck to see how the business is tracking against her original plan. (The company launched mid-2011 and I invested in January of 2012) Often the pitch plan is super ambitious (why shouldn’t it be?) and few companies hit or even exceed it. [Look at Fab.com. I invested in Fabulis – a gay social network – and 18 months later it became a super fast-growing ecommerce site. Bigger and better, most definitely — but very, very different from the original plan. That’s early stage investing. Roll with the punches. Flex with the pivots. Hope for the #win.] In 2012, TheRealReal exceeding its original revenue projections by almost 50%. In 2013, the company really popped – blowing through Julie’s original revenue projections by 350%. 2014 looks to be another stellar year.

Back in ’11 when she was raising seed capital, the investing community didn’t – uh — fully value Julie’s background. She had to hustle, bootstrap and hustle some more to get the company going. Why? She fails the pattern recognition algorithm that (too) many investors use today: She’s experienced. She’s not a technical founder. She didn’t work at Google. She’s a woman. She’s over 50. Those things can count against you in the Valley. Beats me as to why. I found the company on Angelist, met Julie for breakfast (loved her instantly), did a due diligence check the next day at the company’s tiny office/warehouse in a seedy Marin strip mall and quickly pulled out my check book. Julie is super smart, scrappy and determined. She’s an operator. I knew she’d kill it and I couldn’t wait to see investors pounding on her door when she got the company going and that’s precisely what’s happening now.

So what’s the magic formula for TheRealReal?

In addition to a wide selection of luxury products vetted by experts, a great UX and terrific service, it’s three things: 1) Excellent leadership; 2) A great business model; 3) Superb execution.

Leadership: Julie is a seasoned leader. She knows ecomm cold. This is not her first rodeo. I like that in a founder although most of the companies I invest in have first-time — maybe second-time — CEOs. She has disaggregated the business into all the important economic drivers and has developed metrics for each one. She holds her team (and herself) accountable for every metric. If there’s a miss its clear why it happened, who’s responsible and what’s going to be done to fix it. Julie has built a culture about delivery. Set a goal. Deliver.

Business model: TRR brings in merchandise from consignors, vets it to ensure authenticity, styles and photographs it, writes descriptions, loads the product up on the site, collects and fulfills orders then cuts consignors a check when an item is sold. The average transaction size is about 6x a typical ecommerce company (you read that right) and the annual customer value is off the charts. Take Zulily — which is a good public market comp — and add a zero to the annual customer value reported in their S1 and you have the TheRealReal. Really. How the hell?! Look at the brands (Chanel, Hermes, Louis Vuitton). Look at the average price point (couple of hundred dollars). Look at the target customer (well-heeled women). That’s your answer. Plus many buyers are also consignors — which creates a virtuous cycle of consumption and consignment. There is NO working capital tied up in inventory (it’s a consignment model). Last year, I visited the new warehouse and saw very little merchandise. I said, “uh, Julie, where’s all the product?” Her reply, “Mark we often sell through 80% in the first 24 hours a sale is live on the site and we have to pick and pack from the photo studio.” That’s called inventory spin, not inventory turn. With a *huge* average order size, efficient customer acquisition and little working capital, the unit economics are…well…luxuriant…maybe even decadent. Julie is building a powerful brand in the luxury segment and she’s taking the top off Ebay.

Execution: Everyone knows and says ecommerce is all about execution. It’s true. Everyone is assigned goals and they deliver. When there’s a problem it gets fixed. Quickly. The company has scaled nicely without major hiccups – remarkable in ecommerce.

I predict (humble brag?) that this company will pop out of the shadows soon and you’ll see it for the unicorn it’s becoming.

PS The Hermes bag and the two pieces of art presented are available on TheRealReal.com at the time this post was published.